|

|

NSF Resources of Illinois is an

authroized agent of

|

![]()

![]()

![]()

![]()

![]()

|

|

|

Click Below Free Electronic Check Recovery

|

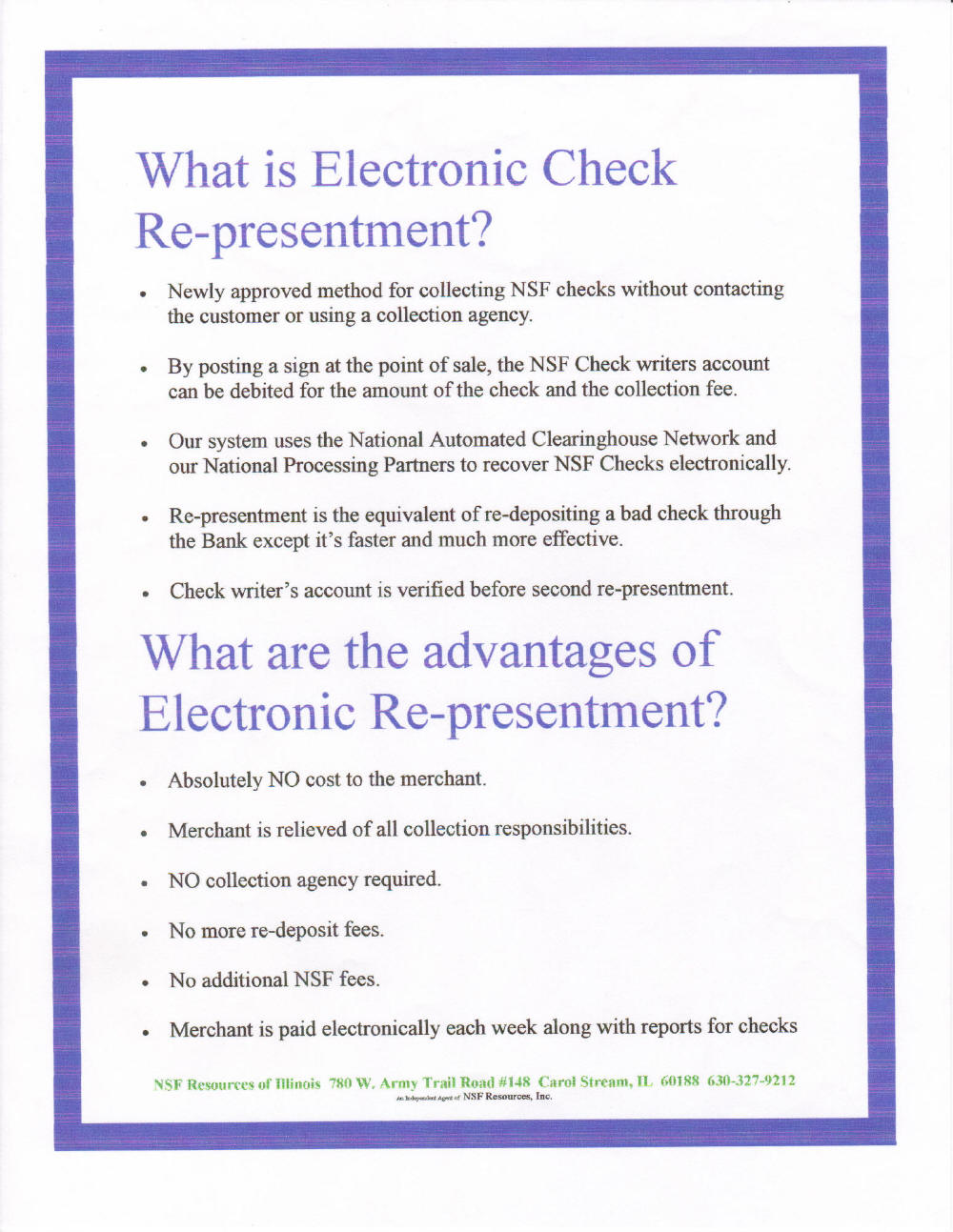

What is Electronic Check Re-presentment?

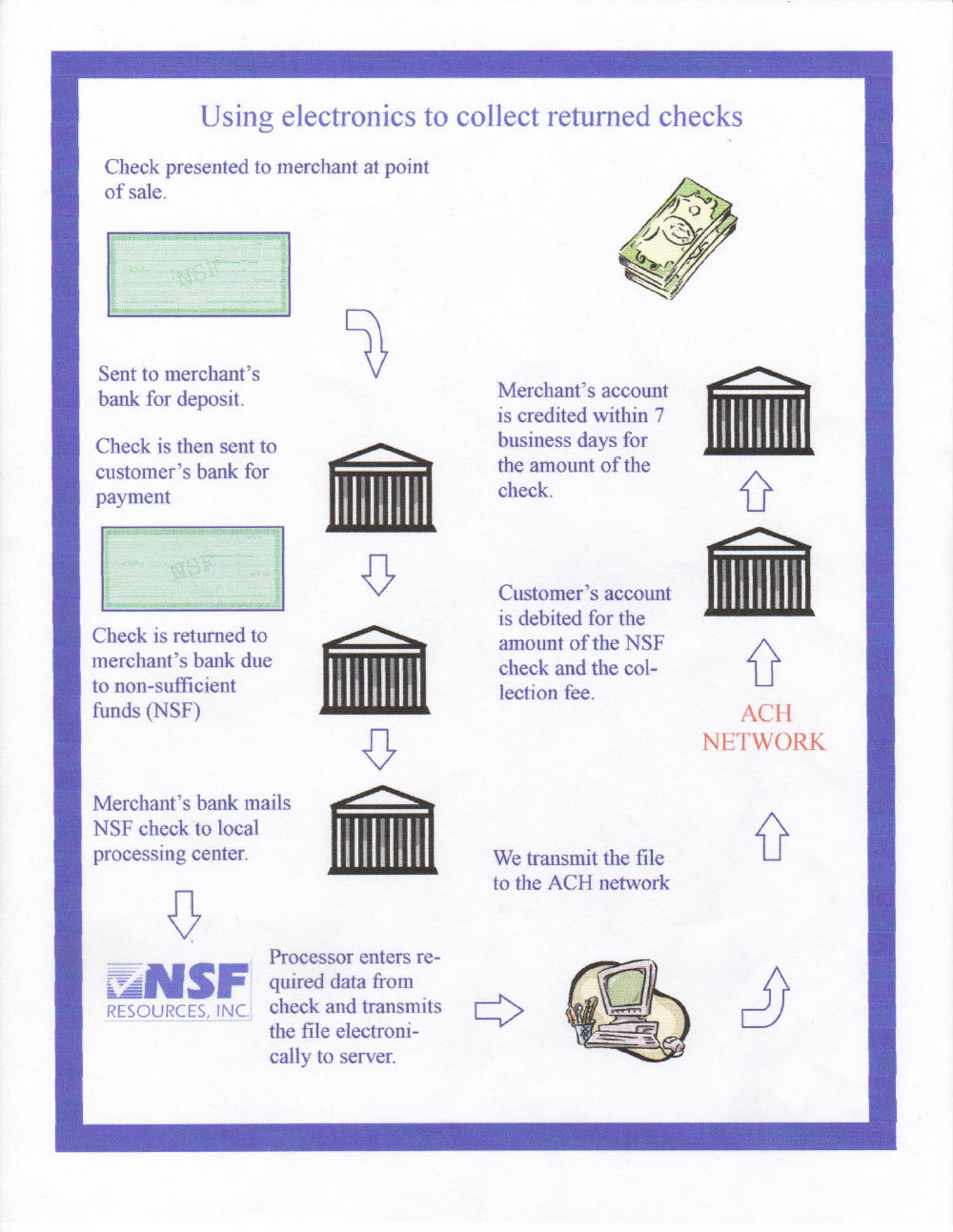

Click images to enlarge. Using Electronics to Collect Returned Checks

THE CHECK COLLECTION PROCESS Brief History The paper check is one of the world's oldest forms of payment, and today exists as one of the most common methods of payment in both the United States and internationally. The traditional check is a debit payment instrument that is widely accepted and used by businesses, governments, and consumers as payment for virtually any form of commerce. In the mid-nineteenth century, reliance on the check as a means of payment increased dramatically as state-chartered banks sought to avoid a Federal tax on banknotes. This growth was supported by the development of clearing houses in several major cities. The clearing house movement demonstrated that checks could be cleared among closely-situated member institutions efficiently, with the legal rights and responsibilities of various parties to a check clearly defined. Over time, the continuing development of the clearing house movement, the creation of the Federal Reserve Bank system in 1913 and subsequent development of the Federal Reserve District infrastructure virtually eliminated all barriers to universal acceptance of the check as a primary means of payment throughout the country. Beginning in the latter half of the twentieth century, significant technological advances were made, the most important of which was the development of automated check processing machinery with the ability to accurately and efficiently process millions of items per day. The automation of check processing has evolved significantly due to the development by the private sector of two important banking industry conventions: (1) a routing number policy adopted by the American Bankers Association in 1911, which transformed local clearing house member identification numbers into a national standard for uniquely identifying any depository institution on which a check is drawn; and, (2) a national standard for imprinting checks with machine-readable numbers and characters in magnetic ink (known as "magnetic ink character recognition", or MICR).1 Since the 1970's, many payment applications (e.g., salary and benefit payments) traditionally handled by check processing are now being processed largely through the use of ACH payments. The growth in check volume for these applications has either leveled off or begun to decline. Nonetheless, developments in check technology such as electronic check presentment, image technology, and financial institutions-to-customer information links, help to ensure the continued life of the check as a primary means of payment well into the next century. Of the estimated 64.6 billion checks written in 1997, approximately 30 percent re-presented "on-us" items; i.e., checks deposited with the paying bank. Inter-bank collection volume, therefore, equates to about 45.2 billion items. Of this total, the Federal Reserve Banks cleared 15.9 billion (up from 15.5 billion in 1996) for a share of about 35 percent of the market. Comparatively, 27.9 billion inter-bank items were cleared privately through either direct sends, correspondent relationships, or for the vast majority, clearing houses. The six clearing houses represented on the Board of Directors of the National Organization of Clearing Houses (NOCH) account for approximately 10 percent of the total inter-bank market (not including items presented at NOCH member clearing houses by a Reserve Bank)3. other clearing houses, in total, represent a large majority of the remaining inter-bank market, with a smaller portion accounted for by direct and correspondent exchanges. Check volume is projected to grow at an annual rate greater than 1 percent into the next century, although industry consolidation may be reducing inter-bank volume and the number of institutions that handle any given inter-bank item through the collection stream. Participants

Typical Transaction Flow Elements of the Check-Clearing System Payer (writes check) Payee (receives check)

Step 1: Company A [the "Payer"] prepares and mails a check to Company B [the "Payee"]. Step 2: Company B receives and processes the check. This includes entering the amount on its cash ledger and crediting Company A's account. Step 3: Company B deposits the check in its account at Bank B. Step 4: Bank B processes the check and either transports it directly to Bank A [go to Step 6] or to a clearing system. A clearing system can be a Federal Reserve Bank, a correspondent bank, or a clearing-house. Step 5: The clearing system gives value to Bank B in the amount of the check and subtracts value from Bank A for the same amount. Step 6: The check is physically presented through the clearing system to Bank A where the amount is deducted from Company A's account. This step may occur simultaneously with step 5. Step 7: Bank A posts a debit to Company A's account. This step does not come at a predetermined time in the cycle since checks are not value-dated for settlement purposes. On the day of posting, company A must have funds available in Bank A to cover the amount of the check or the check may be returned. Step 8: Both financial institutions provide reports to their respective companies in the form of periodic statements and/or daily deposit reports. Clearing Process There are two basic forms

of check collection cycles: on-us checks and transit checks. On-us checks are A transit check may be collected by several different means. These collection mechanisms include clearing houses, the Federal Reserve Banks, and presentment directly to the paying bank or through a correspondent bank. It is common to find that two or more of these mechanisms may be employed to collect one check, (e.g., a check is presented to a correspondent bank which, in turn, exchanges the check through its clearing house.) Legal Framework Uniform laws governing checks and check collection have existed in the United States for many years. From 1896 until the development of the Uniform Commercial Code (UCC) in the 1950s, the Negotiable Instruments Law governed. In addition, many states adopted the Bank Collection Code. The 1962 version of the UCC (with some variations) was adopted by all fifty states. Article 3 of the UCC governs checks while Article 4 governs check collection. UCC Article 4 was amended in 1990 by the American Law Institute and the National Conference of automated processing of checks. At the time of this writing, Revised Article 4 (1990 Official Text) has been adopted by all states except Massachusetts, New York, Rhode Island, and South Carolina. Regulation CC, which was adopted by the Federal Reserve Board in 1988 to implement the Expedited Funds Availability Act, also governs certain aspects of the check collection process. Regulation J and individual Federal Reserve Bank operating circulars govern the check collection process when a Federal Reserve Bank is used. The ACH movement began in the early 1970s when a group of California bankers formed the Special Committee on Paperless Entries (SCOPE). In direct response to the rapid growth in check volume, the Committee was chartered to explore the technical, operational, and legal framework necessary for an automated payments system. SCOPE laid the groundwork for the first Automated Clearing House (ACH) association which began operation in 1972. The establishment of this ACH association led to the formation of similar groups in other parts of the country. Agreements were made between the emerging regional ACH associations and the regional Federal Reserve Banks to provide facilities, equipment, and staff to operate regional ACH networks. Two notable exceptions to this type of arrangement occurred in New York and Chicago, where private clearing houses were formed to handle ACH transactions. In 1974, the National Automated Clearing House Association (NACHA) was formed to coordinate the ACH movement nationwide. Through the joint efforts of NACHA and the Federal Reserve System, local ACHs were linked electronically on a nationwide basis in 1978. The main benefits associated with the use of the ACH Network are cost reduction and improved productivity over paper check transactions. ACH Operators may be private companies or the Federal Reserve Bank (FRB). The current private sector ACH Operators are the American Clearing House Association, the New York Automated Clearing House, and VisaNet ACH Services. ACH Operators are responsible for editing electronic entries received from other ACH Operators or Originating Depository Financial Institutions (ODFIs), submitting them for processing, and for providing settlement between the ODFIs and Receiving Depository Financial Institutions (RDFIs). ACH Operators are linked together for transaction exchange and provide a nationwide ACH system accessible to all depository financial institutions. In an effort to improve the payments system, Congress enacted the Monetary Control Act in 1980. As a result of the Act, private sector ACH Operators were encouraged to compete with the Federal Reserve, which could no longer offer its services free of charge and was required to recover its operating costs. A private sector adjustment factor (I.e., profit margin) is included in Federal Reserve processing so that the Federal Reserve Bank charges as though it were operating on a "for profit" basis. Transactions exchanged between private sector ACH Operators and the Federal Reserve Bank ACH Operator are governed by the interregional deposit and presentment times outlined in Federal Reserve Operating Circulars. Private sector ACH Operators exchange transactions among themselves by deposit and distribution schedules which are established by agreement. NACHA oversees America's largest electronic payments network. NACHA's primary roles are to develop and maintain the NACHA Operating Rules, to promote growth in ACH volume, and to provide educational services to its members and other ACH participants. NACHA's member ACH associations serve over 20,000 financial institutions across the United States, which in turn provide services to over 600,000 corporations and millions of consumers, with an annual transaction volume of nearly 4.5 billion payments and a dollar value of approximately $13 trillion. Regional ACH associations (35 in 1998) provide management, education, assistance, and services to link all types of financial institutions (commercial banks, saving banks, and credit unions) across the United States. Several of these associations also develop and implement local ACH rules that apply to intra-regional ACH transactions. The regional ACH associations offer a wide variety of educational sessions ranging from origination and receipt operations to audit and control. The ACH system is a batch processing , store-and-forward system. Transactions received by the financial institution during the day are stored and processed later in a batch mode. Rather than sending each payment separately, ACH transactions are accumulated and sorted by destination for transmission during a predetermined time period. This provides significant economies of scale. It also provides faster processing than paper checks, which must be physically handled. Instead of using paper to carry necessary transaction information, ACH transactions are transmitted electronically between financial institutions through data transmission. The Returned Check Collection Process Returned check collection in the United States today involves the initiation of check collection activities by one or more entities. The depositor's financial institution, in many cases, may offer to automatically re-present returned NSF items on behalf of the commercial depositor. Some financial institutions also offer return item lock-box services to speed the collection process. Several check verification/guarantee companies also support the merchant's collection efforts after initial efforts at re-presentment have failed. Typically, 40 to 60 percent of returned items are collected on the second presentment. The longer the delay resulting from the physical item being returned to the depository financial institution or to the depositor, the lower the likelihood that the item will be collected. The manual process of holding the checks and then representing them is, at best, inefficient. After the first or second return of the physical check, the commercial depositor or its agent receives the dishonored physical item and the bad check collection process begins. When opportunities for physical re-presentment are exhausted, the depositor or its agent will likely submit the check to the paying bank for manual (non-cash item) collection, or it may deal directly with the maker of the check to obtain payment. The timing of the second presentment is critical. Check verification companies maintain databases (negative files) of accounts known to have outstanding bad checks written against them. These files are accessed by merchants enrolled with the check verification service to mitigate losses from known bad check writers. These proprietary databases are also used to predict the most opportune time for re-presenting a returned NSF item. Check verification/collection companies have found that the sooner the item is re-presented, the greater the likelihood that it will be paid, and the lesser the likelihood of an eventual write-off. Merchants, financial institutions, and consumers benefit from prompt updating of negative files. The sooner the negative file can be updated with bad check data, the sooner the, "bad" check-writer is stopped from writing additional bad checks. More importantly, the sooner a returned check is successfully collected, the sooner the, "good" check-writer's negative file record can be cleared, and the sooner that consumer is, "open to buy". The check re-presentment process has been proven to improve both the speed and timing of NSF check collection, bringing substantial economic benefits to merchants, financial institutions and consumers. THE ACH COLLECTION PROCESS The ACH Network is a processing and delivery system that provides for the distribution and settlement of electronic credits and debits among financial institutions. The ACH Network was developed in response to the astronomical growth of check payments and the many technological advances in the mid-twentieth century and functions as an efficient, electronic alternative to paper checks. Through a nationwide telecommunications network, each ACH Operator is able to communicate with other ACH Operators to exchange entries quickly and efficiently, regardless of geographic distances involved. The ACH Network offers an assortment of technical formats that can be used for a variety of payment applications, products and services. The ACH Network is governed by operating rules and guidelines which are developed by the actual users of the system and is administered through a series of agreements among financial institutions, customers, trading partners, and ACH Operators. Typical ACH Transaction Flow In ACH terminology, Originator and Receiver refer to the participants that initiate and receive the ACH entries rather than the funds. Unlike a check, which is always a debit instrument, and ACH entry may be either a credit or a debit entry. By examining what happens to the Receiver's account, one can distinguish the difference between an ACH credit and an ACH debit transaction. If the Receiver's account is debited, then the entry is an ACH debit. If the Receiver's account is credited, then the entry is an ACH credit. Conversely, the offset to an ACH debit is a credit to the Originator's account and the offset to an ACH credit is a debit to the Originator's account.

ACH credit entries occur when an Originator initiates a transfer to move funds into a Receiver's account. For example, when a consumer uses an automated bill payment service at a financial institution to pay cable access charges each month, the consumer originates the payment through the ODFI which then initiates the credit transaction to transfer the money into the cable company's account; the cable access company is the Receiver. ACH credit transactions involve both consumer and corporate payments with separate rules and regulations for each. The most typical consumer ACH application is Direct Deposit of Payroll.

In an ACH debit transaction, funds flow in the opposite direction. Funds are collected from a Receiver's account and transferred to an Originator's account, even though the Originator initiated the entry. For example, the Originator of a pre-authorized debit is the company to which the amount is owed. Consumers authorize a cable access company to debit their accounts for their monthly bills. Once a month the cable access company initiates a debit file through its ODFI to withdraw the money from the consumers' accounts. The cable company is the Originator, and the consumers are the Receivers. Consumer acceptance is highest in the area of pre-authorized transfers involving regular, recurring payments, such as mortgage payments, installment loans and insurance premiums. Many corporations also use ACH debits to consolidate funds deposited in outlying divisions by operating branches or subsidiaries.

Example: A re-authorized mortgage payment flows from a consumer's account at a financial institution to a mortgage company's account. Figure B also illustrates a corporate cash concentration flow from a company's local or regional financial institution account to a company's regional or national financial institution account. Debit entries must not be posted to a Receiver's account prior to the settlement date. On-Us Entries An "on-us" transaction is one in which the Receiver and the Originator both have accounts at the same financial institution. Therefore, the transaction need not be sent through the ACH Network but instead may be simply retained by the financial institution and posted to the appropriate account. Legal Framework The ACH process operates from beginning to end through a series of legal agreements. Before any transaction is initiated, the Originator and ODFI execute an agreement to use the ACH Network to originate payments. Among other things, the agreement should bind the originating company to the NACHA Operating Rules, define the parameters of the relationship between the two parties, identify processing requirements for the specific applications(s), and establish liability and accountability for procedures related to certain application(s). By participating in the ACH Network, participants agree to abide by the NACHA Operating Rules. The NACHA Operating Rules govern interregional ACH transactions and also cover intra-regional (local transactions) unless a local ACH association has implemented a local rule to supersede a provision of the NACHA Operating Rules. While the NACHA Operating Rules is the primary document covering the rules and regulations for the commercial ACH Network, Federal Government ACH payments are controlled by the provisions of Title 31 Code of Federal Regulations Part 2100 (31 C>F>R> Part 210). The Financial Management Service (FMS) of the U>S> Department of the Treasury is the agency responsible for establishing Federal Government ACH policy. FMS is also responsible for the publication of The Green Book, a procedural manual for Federal Government ACH payments. Other laws which have a direct bearing on ACH operations are the Uniform Commercial Code Article 4, which will govern re-presented check entries, and Article 4A, and the Electronic Funds Transfer Act as implemented by Regulation E. Certain other activities related to ACH payments are affected by The Right to Financial Privacy Act, Regulation D regarding reserve requirements, Regulation CC regarding funds availability, and other regulatory agency directives. Agreements are also required between ACH participants and the ACH Operators for ACH Operator services. Relationships between the consumer as Receiver and the RDFI are generally governed by Regulation E and the NACHA Operating Rules. In some cases, agreements exist between the RDFI and the Receiver, particularly if the Receiver is a corporate or government entity. How Checks Are Re-presented Over the ACH Network - Process Flow Figure C: Re-presented Check Entries Using

Electronics to Collect Instead of the check being re-presented if is returned insufficient or uncollected funds, the new ACH process allows the merchant to re-present the item as an ACH debit. With an ACH debit transaction, the item is converted into an ACH entry and transmitted from the merchant (Originator) to their financial institution (ODFI) to the ACH Operator to the consumer's financial institution (RDFI) in order to debit the consumer's account for the face value of the check. Rule Amendments for Re-presented Check Entries Re-presented check entries are being implemented into the NACHA Operating Rules in two phases: Interim Solution: Using the PPD Format to Re-present Checks The first rule amendment is effective from September 18, 1998 until September 16, 1999. This rule amendment modifies the NACHA Operating Rules to expand the definition of the Pre-authorized Payment and Deposit (PPD) format to allow this format to be used to transmit ACH debit entries in place of a paper check after the paper item is returned or insufficient or uncollected funds. This rule amendment is an interim solution, and can no longer be used after September 16,1999. Although the PPD SEC Code would be used, both the ODFI and the RDFI would be able to identify the re-presented check entry because "REDEPCHECK" would be located in the Company Entry Description Field of the Company Batch/Header Record. In addition, the rules language is exactly the same in the interim solution using PPD as in the RCK amendment: 1) a new SEC code is not being used, 2) the new reasons for return are incorporated into current return reason codes, and 3) the RDFI is not required to print the check serial number to the consumer's statement in the interim solution. Final Solution: Re-presented Check Entries This rule amendment becomes effective on September 17, 1999. The second rule amendment modifies the NACHA Operating Rules to create a new Standard Entry Class (SEC) Code, RCK (Re-presented Check Entry), which will be used to provide commercial depositors and their financial institutions with a method to transmit ACH debit transactions in place of a paper check after the paper item is returned for insufficient funds. This optimal solution establishes a new SEC code, RCK, which will enable ACH participants to clearly distinguish this type of transaction from other ACH transactions, allowing for more efficient compliance with unique rules governing: 1) reasons for returns,20 return time frames, 3) stop payment rules, 4) statement requirements, and 5) customer service issues, among others. Final Rule: Using the RCK Format to Re-present Checks On September 19, 1999 a rule amendment will become effective which modifies the NACHA Operating Rules to create a new Standard Entry Class Code, RCK (Re-presented Check Entry), to provide commercial depositors and their financial institutions with a method to transmit ACH debit transactions in place of a paper check after the paper item is returned for insufficient funds. Legal Framework RCK entries will be subject to the applicable NACHA Operating Rules, the Uniform Commercial Cod (UCC), and Federal Reserve Regulation CC, but not to the Electronic Funds Transfer Act or Regulation E. The legal framework for the RCK is premised on the fact that the origin of each RCK entry is a paper check that has been dishonored. Transfers of funds that were "originated by a check, draft or similar paper instrument," are specifically excluded from coverage under the EFTA (15 U>S>C> 1693a(6)) and Regulation E (12C>R>R>205.3©(1). Accordingly, if an RCK entry is treated as a check transaction for purposes of the EFTA and Regulation E, then it is logical that the UCC and Regulation CC should continue to be the body of law that governs the rights and responsibilities of the parties involved with that payment, even though it has been converted to electronic form. Rules Framework The RCK transaction will provide for a method for the depositor or its agent to transmit an ACH debit entry to present the item (check) in electronic form, when either the first or second physical presentment of the item (check) is returned for not sufficient funds. Eligible Items In order to be eligible to be transmitted as an RCK entry, the check must:

Number of Presentments Allowed An RCK entry can be transmitted either after one physical or two physical presentments of the item (check). The RCK entry can be sent twice if there was only one previous physical presentment and one time if there were two physical presentments. Ineligible Items Items that are ineligible for transmission as re-presented check entries include, but are not limited to:

Restrictive Endorsements If a depositor or its agent has placed a restrictive endorsement (e.g., "For Deposit Only") on the check, the restrictive endorsement would be ineffective or void when the check is presented as an RCK entry. It is the Originator that initially places the restrictive endorsement on the item and subsequently chooses to re-present it as an RCK entry, and ODFI will be unable to physically examine the item to identify restrictive endorsements.

Originators of RCK entries will be required to provide notice to the check writer, prior to receiving an item to which an RCK entry relates, informing the check-writer that his returned item may be collected electronically if the check is returned for insufficient funds. The manner in which the Originator provides notice will not be prescribed in the NACHA Operating Rules, stating instead that the notice must clearly and conspicuously state the terms of the RCK policy before the Originator receives the item to which the RCK entry relates. The NACHA Operating Guidelines contain the recommendation that (1) if notice is provided at the point-of-sale, it must be contained on a sign at the point-of-sale, and (2) if notice is provided by a billing firm (i.e., utility or credit card company which issues a bill for payment), the notice will be contained on the monthly billing statement. To protect both the check-writer and the RDFI, a check-writer will be able to sign an affidavit at his RDFI if the required notification by the Originator was not provided and have his account re-credited. The RDFI, in turn, will be able to return the RCK entry (for which the check-writer has signed an affidavit that notice was not provided) by transmitting the return entry to its ACH Operator by its deposit deadline for the return entry to be made available to the ODFI no later than the opening of business on the banking day following the sixtieth calendar day following the settlement date of the RCK entry. Both the RDFI and the check-writer are protected in cases where the originator did not provide proper notice that an RCK entry would be transmitted and the Originator is protected by having RCK entries returned for "Notice Not Provided" only if the check-writer signs an affidavit. Collection Fee Not Included in thr RCK Entry RCK entries may only be transmitted for the face amount of the item (check). No collection fees may b e add to the amount of RCK entry. Return of and RCK Entry For most RCK returns, the RDFI will need to transmit a return entry to the RDFI's ACH Operator by midnight of the second banking day following the banking day of receipt of the presentment notice (e.g., the RCK entry) (see Diagram2). The presentment notice is deemed to be received when the ACH Operator makes the RCK entries available to the RDFI. This RCK return time frame is different from the typical ACH return time frame because of the need to be consistent with return time frames under the Uniform Commercial Code (UCC). The typical ACH return time frame requires that the return entry be received by the RDFI's ACH Operator by its deposit deadline for the return entry to be made available to the ODFI no later than the opening of business on the second banking day following the settlement date of the original entry (see Diagram1)

BACKGROUND - RE-PRESENTING CHECKS OVER THE ACH NETWORK Almost twenty years ago, the American Bankers Association established a task force to develop a product that would permit a check to be truncated and converted into an ACH transaction at the bank of first deposit. Operating rules, new formats and marketing and educational material were produced to implement and promote the product. Unfortunately, the marketplace never embraced the product because there was no business case for the bank of first deposit or its customers to incur the product development costs. Almost 20 years later, a truncation product has finally been developed with a compelling business case that will yield substantial benefits to financial institutions and their customers. In April 1995, NACHA

established the Electronic Check Council to develop products that would allow

checks to be processed and collected using electronic payment networks. Council

members include representatives from most of the major stakeholders in the check

collection business: banks, clearinghouses, retailers, remittance processors,

billers and the check verification and guarantee companies. After developing a

Pilot Operating Guide in the fall 1996, the Council sponsored a NACHA Rules Work

Group to develop the rules framework for re-presenting checks. The Council &

Rules Work Group has now completed its work on a product that uses the ACH

Network to represent checks that have been returned unpaid. Overall Benefits of RCK

Merchant Benefits: Retailers have begun using the ACH Network to test the feasibility of the re-presented check entry concept and have experienced promising results. It is estimated that currently 3000-6000 retailers are using the ACH Network to transmit entries to re-present checks. In these tests, the retailer, to whom a check is returned for insufficient funds, converts the check into an ACH debit rather that re-depositing the physical check through the check collection system. The retailers testing the electronic re-presentment concept report substantially reduced costs and higher collection rates than achieved using the paper check clearing process. Retailers are saving processing costs of 25 to 50 cents for every check converted and are experiencing up to 50 percent higher collection rates. These significant improvements are the result of two factors. First, retailers can target the exact date an ACH debit will be charged to an account using models that predict when the check writer has higher balances in the account. Second, because the cost of creating an ACH debit is much lower than the cost of re-depositing the physical check, small-value checks can now be collected cost effectively. Financial Institution Benefits: Every financial institution receives checks from its customers - whether for credit card, mortgage, automobile, home equity or other payments. In many cases, these checks are drawn on accounts the check writer has with another financial institution. The same benefits described above for retailers will also be realized by financial institutions when they convert a check that has been returned unpaid into an ACH debit. The RDFI will experience operating cost savings whether the ACH debit is paid or is returned unpaid. If the ACH debit is returned unpaid, the RDFI will save between 25 cents and $1.00 per transaction. These savings are based on the difference in the price the Federal Reserve charges for an ACH return compared to a check return. This estimate is conservative because it assumes that the cost to the RDFI to prepare an ACH return is the same as the cost of preparing a returned check. Financial institutions that have automated the ACH return process will save even more. Also, for every ACH debit that is paid, there will be one less check to be included in the monthly statement, resulting in lower postage expenses. Consumer Benefits Use of the ACH Network to re-present checks which have been returned for insufficient or uncollected funds will result in quicker, more efficient collection of NSF checks enabling check verification systems to remove negative file records that have been placed against consumer's accounts more quickly. The quicker the removal of negative consumer files, the quicker the consumer is again free to make purchases via check.

| |||||||||||||||||||||||||||||||||||||||||||||||||

|

Send mail to

nsfresources@sprynet.com with

questions or comments about this web site.

|